The European hotel investment market has entered a new phase defined by disciplined capital deployment, selective underwriting and active asset management. Investor sentiment remains constructive, and conviction in travel demand fundamentals is strong. However, a critical disconnect has emerged between robust top-line operating performance and deteriorating bottom-line profitability. The “scissor effect” of rising costs—particularly payroll outpacing revenue growth is compressing GOP margins and forcing investors to re-evaluate return assumptions. Hurdle rates have risen meaningfully, and institutional capital is no longer willing to transact at legacy peak-cycle pricing. Transaction volumes have nonetheless reached their highest levels since the pre-pandemic period, driven overwhelmingly by single-asset deals where buyers see clear operational value-creation upside and immediate returns.

The market’s direction is being shaped by converging structural trends that will define the investment landscape through the end of the decade. First, luxury and extended-stay segments are commanding disproportionate capital flows—luxury benefits from structurally constrained supply, pricing power and a growing UHNW traveller base, while extended stay offers superior GOP margins, lower operational complexity and alignment with hybrid work and longer-stay travel patterns. Second, the generational transition of family-owned hotels across Southern Europe is expected to create one of the largest transaction trends in decades—a multi-year pipeline of well-located, underinvested assets ripe for institutional repositioning. Third, family offices have become a dominant force, now accounting for roughly 14% of hotel transactions, leveraging their permanent capital structures and operational flexibility to outmanoeuvre traditional private equity funds in a bid–ask-constrained market. Fourth, branded residences are emerging as a critical enabler for luxury development, providing upfront capital recovery, de-risking projects and commanding 20–35% pricing premiums.

Looking ahead, the European hotel sector’s trajectory points towards continued volume growth—but the winners will be determined by execution capability rather than market beta. The era of passive yield compression and leverage-driven returns is effectively over. Supply remains disciplined and development economics are increasingly pushing capital towards conversion and adaptive reuse strategies over ground-up builds.

On the debt side, regulatory frameworks are tightening traditional bank lending, supporting the growth of private credit but also introducing refinancing risk that demands rigorous underwriting. CEE markets are transitioning from fringe to core investment geographies, while Western and Southern Europe offer defensive positioning. The bottom line: this is a market that rewards active operators and investors, deep expertise and total asset optimisation. While growth projections remain positive, underlying volatility means that success will increasingly depend on expertly crafted capital stacks that support investors, lenders and operators through downside scenarios. Those who can bridge the gap between strong demand fundamentals and the operational challenge of converting revenue into profit will capture outsized risk-adjusted returns across what remains one of Europe’s most compelling real estate asset classes.

Investor Sentiment

Demand confidence intact, return expectations softening — and the gap is the signal

The European hotel investment market entered 2026 with a notable sense of calibrated readiness. Capital availability remains strong, and conviction in the long-term fundamentals of travel demand is firmly intact. However, what has fundamentally shifted is investor pricing discipline. Unlike previous years, institutional capital is no longer chasing deals indiscriminately, and investors are increasingly unwilling to transact based on legacy pricing benchmarks formed during peak-cycle conditions.

Investor sentiment reflects this more measured stance. The Hospitality Investor Sentiment Index stands at 59 in Q1 2026, maintaining a broadly positive outlook but retreating from the highs observed during 2024–2025. Beneath this headline figure, more telling dynamics emerge. Most notably, hurdle rates have increased significantly, signalling that investors are demanding higher returns before committing capital. This shift does not indicate a lack of confidence, but rather a more selective and strategic approach. Investors are prepared to wait for opportunities where pricing aligns with risk or where operational upside can be clearly identified and executed.

Investor conviction remains strong, but capital is now deployed with discipline precision and a clear focus on risk adjusted returns.

At the same time, ESG considerations while still structurally embedded in the market are undergoing a tactical reprioritisation. The decline in ESG emphasis within asset management strategies suggests that, in the current environment of cost pressures and geopolitical uncertainty, sustainability has shifted from a primary value driver to a baseline requirement. Nevertheless, ESG remains deeply integrated at the institutional level, particularly through fund mandates and lending frameworks. With upcoming regulatory frameworks such as the EU’s Corporate Sustainability Reporting Directive (CSRD), ESG factors are likely to regain prominence, particularly as they begin to influence asset liquidity, valuation, and access to financing.

A key theme shaping the investment landscape is the growing disconnect between operational performance bottom line and investor return expectations. While confidence in hotel demand and trading performance remains strong, this optimism is no longer translating directly into confidence in equity returns, especially in passively managed asset. The underlying issue lies within the capital structure: rising interest rates, refinancing risks, evolving exit yield assumptions, and cost inflation - particularly in labour are all placing pressure on profitability conversion.

As a result, even assets demonstrating solid RevPAR growth may struggle to deliver the returns required by today’s more disciplined investors.This evolving dynamic marks a clear transition in the market from a recovery-driven environment to one defined by selectivity and underwriting precision. The broad-based competition for assets seen in the post-pandemic recovery phase is giving way to a more nuanced approach, where investors differentiate sharply between opportunities. Assets with clear operational value creation potential, strong branding, and resilient demand drivers will continue to attract capital. Importantly, despite this increased selectivity, the sector’s forward outlook remains positive. Hotel investment volumes are projected to grow by over 33% between 2026 and 2030, reinforcing the asset class’s long-term attractiveness within a diversified real estate portfolio.

Europe's Hotel Demand Growth

From recovery to structurally supported expansion driven by global travel growth

European hotel demand has moved decisively beyond the recovery phase and into a structurally supported growth cycle. By the end of 2025, international arrivals across Europe reached approximately 106% of 2019 levels, clearly surpassing pre-pandemic benchmarks. Southern Europe continues to lead this recovery, exceeding 110%, followed closely by Western Europe, while Northern and Central & Eastern Europe have now broadly normalised. These areas are also expected to have largest growth in the coming years. On a global level, the recovery remains uneven but positive, with the Middle East significantly outperforming and Asia-Pacific still catching up. This divergence reinforces Europe’s position as a near-term beneficiary of reallocated global travel flows, particularly as long-haul travel patterns continue to normalise.

A key structural driver behind this growth is the continued expansion of the global travelling population. Hundreds of millions of new travellers - particularly from emerging markets - are entering the international tourism ecosystem, driven by rising incomes, increased passport ownership, and improved air connectivity. This trend not only strengthens traditional European gateway cities but also creates new demand pools for secondary destinations. For investors, this represents a dual opportunity: capturing inbound demand from new source markets while also identifying emerging destinations within Europe that can absorb and monetise this growth.

Importantly, the recovery is broad-based across all travel segments, dispelling earlier concerns about structural demand impairment. Leisure travel has been the primary driver, already exceeding pre-pandemic levels and continuing to grow, but business travel has also returned to growth, surpassing 2019 levels and demonstrating renewed relevance. While the nature of corporate travel has evolved - characterised by more flexible travel patterns, longer stays, and increased blending of business and leisure - the overall volume has recovered. This evolution supports alternative accommodation formats, extended-stay products, and lifestyle-oriented hotel concepts, all of which are increasingly attractive from an investment perspective.

However, the aviation outlook introduces an important constraint to future growth. While passenger volumes in Europe are expected to increase significantly over the long term, the pace of growth is projected to slow compared to the pre-pandemic decade. Structural factors such as sustainability regulations, aviation fuel requirements, and airport capacity limitations - particularly at major European hubs - are likely to cap supply expansion. This creates a fundamentally supportive environment for hotel performance, as constrained air capacity can translate into pricing power for both airlines and accommodation providers, particularly in high-demand destinations with limited new hotel supply.

At the same time, geopolitical dynamics continue to shape short-term demand flows. Ongoing tensions in the Middle East, for example, have already resulted in a reallocation of leisure demand toward Southern European destinations such as Spain, Italy, Portugal, and Greece. This highlights the adaptability of global travel demand and the importance of geographic diversification in hotel investment strategies. While the underlying demand drivers—such as experiential travel, climate preferences, and lifestyle shifts remain highly resilient, the composition of that demand will continue to evolve. For investors, the key will be identifying not just where demand exists, but how it is changing, and aligning asset strategies accordingly to capture outsized performance.

High-Growth Hotel Markets & Demand Shifts

A diverse landscape where emerging CEE markets drive growth while established destinations provide stability and pricing resilience

European hotel demand has moved decisively beyond the recovery phase and into a structurally supported growth cycle. By the end of 2025, international arrivals across Europe reached approximately 106% of 2019 levels, clearly surpassing pre-pandemic benchmarks. Southern Europe continues to lead this recovery, exceeding 110%, followed closely by Western Europe, while Northern and Central & Eastern Europe have now broadly normalised. These areas are also expected to have largest growth in the coming years. On a global level, the recovery remains uneven but positive, with the Middle East significantly outperforming and Asia-Pacific still catching up. This divergence reinforces Europe’s position as a near-term beneficiary of reallocated global travel flows, particularly as long-haul travel patterns continue to normalise.

A key structural driver behind this growth is the continued expansion of the global travelling population. Hundreds of millions of new travellers - particularly from emerging markets - are entering the international tourism ecosystem, driven by rising incomes, increased passport ownership, and improved air connectivity. This trend not only strengthens traditional European gateway cities but also creates new demand pools for secondary destinations. For investors, this represents a dual opportunity: capturing inbound demand from new source markets while also identifying emerging destinations within Europe that can absorb and monetise this growth.

Importantly, the recovery is broad-based across all travel segments, dispelling earlier concerns about structural demand impairment. Leisure travel has been the primary driver, already exceeding pre-pandemic levels and continuing to grow, but business travel has also returned to growth, surpassing 2019 levels and demonstrating renewed relevance. While the nature of corporate travel has evolved - characterised by more flexible travel patterns, longer stays, and increased blending of business and leisure - the overall volume has recovered. This evolution supports alternative accommodation formats, extended-stay products, and lifestyle-oriented hotel concepts, all of which are increasingly attractive from an investment perspective.

At the same time, established markets such as Switzerland and the broader Scandinavian region present a compelling and complementary investment case, centred on stability, long-term growth potential, and strong pricing power rather than rapid expansion. Switzerland, in particular, benefits from resilient inbound demand and high barriers to entry, which support consistent performance across economic cycles, while similarly strong fundamentals—political stability, transparency, and limited supply growth characterise key Nordic markets.

Traditionally renowned as a premier winter destination, Switzerland—like the broader Alps has increasingly evolved into a year-round market. This shift is mirrored across Scandinavia, where countries such as Sweden, Denmark, Norway, and Finland are experiencing growing summer demand. Driven by the “coolcation” trend, travellers are increasingly seeking milder climates, nature-based experiences, and relief from extreme heat in Southern Europe. As a result, both regions are seeing improved seasonality profiles and more balanced annual performance.

In the current macroeconomic environment, where capital preservation and downside protection are key priorities, these characteristics position Switzerland and Scandinavia as defensive and highly attractive markets for institutional investors.

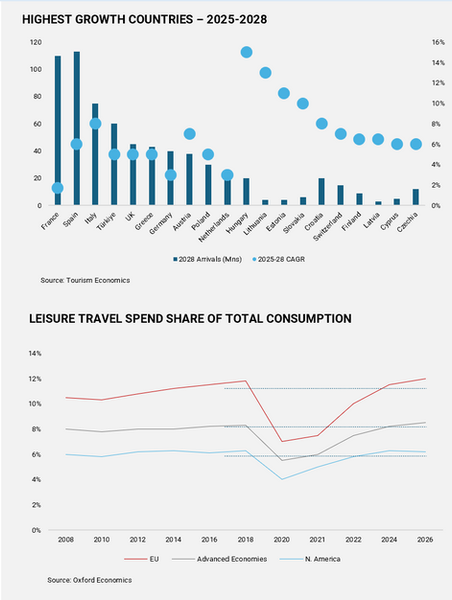

On the demand side, the evolution of leisure travel spend provides important insight into long-term consumption patterns. Leisure travel expenditure as a share of total consumption has not only recovered following the pandemic but is now trending above pre-2020 levels, particularly within Europe. This reflects a structural shift in consumer behaviour, where travel and experiences are increasingly prioritized over traditional goods-based consumption. As a result, the long-term demand outlook for hotel assets remains robust, supported by both domestic and international travel flows.

Importantly, Europe is outperforming other advanced economies in this regard, with leisure spend share exceeding both North America and the broader advanced economies benchmark. This divergence highlights the strength of intra-European mobility, the continued recovery of long-haul travel, and a broader lifestyle-driven shift toward experiential spending. While macroeconomic pressures—particularly on the middle class remain a consideration, current behaviour indicates a sustained willingness to allocate income toward travel. However, investors should remain mindful that in a more severe downturn scenario, discretionary spending on travel may eventually soften. Nonetheless, in the base case, the European hotel sector remains well-positioned to deliver both occupancy and ADR growth, reinforcing a strong and balanced investment thesis across the region.

Supply Overview

Moderate, high-end skewed, and constrained by the costs that make existing assets valuable

The hotel supply dynamics remain disciplined, uneven, and highly segment-driven creating a structurally supportive environment for existing assets while simultaneously challenging new development feasibility, especially when development timelines are expanding, hence increasing pressure on investors’ return projections. While overall supply growth across major European cities is expected to increase modestly from around 2% in 2025 to approximately 3% in 2026, this headline figure masks a clear divergence by segment. Luxury leads projected growth at 4.5%, followed by upper midscale and economy segments, while midscale and upper upscale lag behind. This skew reflects a fundamental shift in development economics: segments with stronger pricing power and higher RevPAR potential are better positioned to absorb rising construction and financing costs, whereas more cost-sensitive segments face increasing margin compression. It is also notable that luxury and upper-upscale might attract more family offices and HNWI investors who are looking for legacy hotels and have notable longer holding periods and different return metrics.

At a city level, supply conditions vary significantly, reinforcing the importance of micro-market selection. Selection of cities are seeing elevated pipeline activity, while some traditional gateway markets remain heavily supply-constrained due to regulatory, physical, and political barriers. This imbalance creates localized pockets of opportunity and risk. For example, constrained markets continue to benefit from strong pricing power and limited competitive pressure, while higher-growth cities may experience short-term supply absorption challenges, albeit often supported by strong underlying demand fundamentals.

Looking at the broader European pipeline, development activity remains substantial but increasingly uncertain in execution. Over 2,200 new hotels are expected to come to market in the coming years. However, a significant proportion of these projects remains in planning or early-stage development, where financial viability is most exposed to cost inflation and financing conditions.

This environment is accelerating a structural shift away from ground-up development toward conversion and adaptive reuse strategies. Investors and developers are increasingly targeting existing buildings—particularly offices, heritage assets, and underutilized real estate that can be repositioned into hospitality assets at a lower cost basis than new construction in prime locations. Beyond cost efficiency, these projects benefit from shorter development timelines, lower environmental impact, and stronger narrative-driven positioning. In a market where authenticity and experience are key demand drivers, such assets often outperform standardized new-build product, particularly in urban and lifestyle-driven destinations.

In parallel, the extended-stay segment is emerging as a key growth area within the European supply pipeline. With a growing share of total development and increasing brand participation from major global operators, this segment reflects evolving guest preferences toward flexibility, longer stays, and hybrid travel patterns. However, despite strong brand expansion, market fragmentation remains high, and scale is still limited compared to more mature regions. This creates a clear consolidation opportunity for institutional capital, particularly for platforms capable of executing cross-border strategies and building operational scale.

Overall, Europe’s hotel supply story is no longer about volume expansion, but about strategic positioning—favouring investors who can navigate complexity, identify mispriced opportunities, and align product with evolving demand patterns.

Transactions

Rising transaction activity driven by single asset deals geographic diversification and a shift toward operational value creation

The European hotel transaction market has re-established strong momentum, with 2025 marking the most active year since the pre-pandemic peak. Total transaction volume reached €22.6 billion*, reflecting a significant rebound and reinforcing investor confidence in the asset class. Notably, single-asset transactions drove this recovery, reaching a record €15.6 billion* and highlighting a clear preference among investors for granular, asset-level opportunities where operational upside can be actively executed. Portfolio transactions remained stable, suggesting that while large-scale platform trades persist, the market is currently more focused on selective acquisitions rather than broad portfolio repositioning.

Geographically, the market continues to be led by its traditional core - France, the UK, Spain, and Germany, but with notable differentiation in performance drivers. France emerged as the standout growth market, supported by strong domestic demand fundamentals and a favourable regulatory and tax environment for hotel ownership. The UK maintained its position as one of Europe’s deepest and most liquid markets, while Spain continued to benefit from its global tourism appeal. Germany’s recovery is particularly noteworthy, signalling renewed investor confidence in a market that had lagged in the immediate post-pandemic period. However, structural challenges remain, particularly within its traditionally conservative operating environment, where higher cost structures, regulatory complexity, and slower operational flexibility continue to weigh on performance and investment underwriting. This is further compounded by the market’s strong preference for fixed lease structures, which, while offered in the past income security are not strong as before. Together, these markets form the backbone of European hotel liquidity, providing scale and consistency for institutional capital deployment.

At the same time, secondary and emerging markets are playing an increasingly important role in shaping the investment landscape. Countries such as Greece, Italy, the Czech Republic, Austria, Ireland, and Portugal are attracting growing volumes of capital, reflecting a broader geographical diversification of investor activity. This shift is supported by improving market transparency, stronger tourism fundamentals, and the availability of repositioning opportunities.

Cities like Athens and Prague, in particular, have demonstrated their ability to absorb substantial investment volumes, highlighting the continued institutionalisation of previously less mature markets.

Despite strong demand for hotel assets, transaction activity remains constrained by a persistent bid-ask spread. While capital availability is high and investor appetite remains robust, pricing expectations between buyers and sellers are not always aligned. This dynamic is further influenced by evolving financing conditions. Although lending markets have become more supportive with tighter spreads and higher loan-to-value ratios - debt availability alone is not sufficient to bridge valuation gaps. As a result, deal flow is increasingly dependent on motivated sellers or situations where pricing reflects realistic underwriting assumptions rather than peak-cycle benchmarks.

Looking ahead, successful deals are no longer defined purely by financial engineering but by a clear operational or strategic thesis. Owner-operators, family offices, and long-term capital providers are becoming more prominent, focusing on assets where value can be created through active management, repositioning, or brand alignment. In contrast, traditional strategies reliant on leverage and yield compression are becoming more difficult to execute.

Operating Performance

The revenue-cost scissor that sits at the centre of every European hotel investment thesis

Operating performance in 2025 reflects a market where top-line resilience remains intact, but bottom-line pressure is becoming increasingly structural. Revenue performance continues to grow, supported by steady gains in occupancy and ADR, with RevPAR reaching €107, 32% above 2019 levels*. Importantly, demand is not only strong but also broadening across the calendar. This extension of the operating season is a positive structural shift, supporting more stable annual cash flow profiles. Additionally, ancillary revenues - particularly F&B are outperforming rooms revenue, highlighting the increasing importance of total revenue management.

However, this revenue growth is being consistently outpaced by rising operating costs. Total expenses grew faster than revenue, with payroll emerging as the primary pressure point. As the largest cost component, payroll increased significantly, driven by structural labour shortages, wage inflation, and operational inefficiencies in certain markets. Other cost lines, including sales and marketing and departmental overheads, also continue to rise, while temporary relief from lower utility costs remains fragile in the face of geopolitical risks. The result is a compression of profitability, with GOP growth lagging behind revenue growth.

This dynamic is clearly reflected in declining operational efficiency. GOP per available room increased only marginally, while margins have begun to contract. The gap between revenue growth and cost inflation the so-called “scissor effect” is widening, and it is particularly concerning that the most significant cost line is growing at the fastest pace. In this environment, traditional reliance on RevPAR growth alone is no longer sufficient to drive profitability. Instead, operators must actively manage productivity, cost structures, and revenue diversification to protect margins.

Brands have seen strong growth in fee income, particularly driven by the expansion of franchise agreements across Europe, but this trend is expected to enter a more scrutinised phase. As operating margins come under pressure, owners are increasingly focused on the net profitability impact of brand affiliation, questioning whether fees are fully justified by performance uplift. This is likely to push brands to deliver more tangible value beyond distribution and loyalty systems, including stronger support in revenue management, IT management, cost control, and operational efficiency. As a result, the balance of power is gradually shifting, creating a more favourable environment for hotel owners to negotiate terms and fully capitalise on their investments.

Several cities across Europe are experiencing continued growth in Gross Operating Profit per Available Room (GOPPAR), reflecting strong operational performance and resilient demand fundamentals. However, in more mature markets such as London, Edinburgh, and Dublin, the pace of growth is beginning to moderate.

This softening trend should be viewed in context: these cities are already operating at relatively high-performance levels, with well-established demand bases and strong pricing power. As such, a gradual deceleration is not necessarily indicative of weakening fundamentals, but rather a natural progression toward stabilization. It is typical for markets to experience a tapering of growth after periods of strong expansion, eventually reaching a more balanced and sustainable level of performance.

Looking ahead, the margin pressure facing European hotels is unlikely to resolve organically. Structural drivers - such as demographic shifts, labour shortages, and rising service-sector costs - will continue to weigh on operating models. As a result, the competitive advantage will increasingly shift toward operators capable of adapting quickly. Automation, leaner staffing models, and digital optimisation are becoming essential tools, while revenue diversification - across F&B, events, co-working, and mixed-use concepts offers a pathway to enhance asset productivity. The European hotel sector is not facing a demand problem, but an operational one.

4 Key Hotel Segments Driving Investments

Luxury Hotels

Persistent Demand Driving the Appetite

The sustained outperformance of the luxury hotel segment is fundamentally rooted in structural demand drivers that extend well beyond cyclical travel recovery. The affluent and ultra-high-net-worth travellers have demonstrated significantly lower price sensitivity, enabling strong and sustained ADR growth across key global destinations.

This is reinforced by a broader behavioural shift, where luxury consumption is increasingly experience-led rather than product-driven - travel, wellness, gastronomy, and unique, curated experiences have become primary outlets for discretionary spending. At the same time, the global expansion of wealth particularly among high- and ultra-high-net-worth individuals is expected to continue, providing a growing and resilient customer base. Combined with structurally constrained supply, particularly in prime European locations where development barriers are high, this creates a powerful imbalance that supports long-term pricing power and asset value appreciation.

For investors, capitalising on this demand requires a more nuanced and strategic approach than traditional hotel investment models. Firstly, asset selection is critical—focus should be placed on irreplaceable locations, heritage assets, and destinations with strong

international appeal, where barriers to entry protect long-term value especially when the development costs for luxury hotels can increase up to €1m per room, noticeably higher than upper-upscale segment.

Secondly, investors must lean into the evolving nature of luxury demand by prioritising experiential differentiation. Hotels that integrate high-margin, curated experiences whether through wellness, local culture, or bespoke activities can significantly enhance total revenue per guest and improve profitability beyond rooms revenue alone.

Thirdly, mixed-use components such as branded residences offer a compelling financial lever, providing upfront capital, de-risking development, and enhancing overall project returns.

Equally important is the operating and branding strategy. Strong brands remain a key driver of rate premium and global distribution, but investors should structure agreements carefully to ensure alignment and preserve upside.

In some cases, independent or soft-brand strategies may deliver stronger positioning, particularly in markets where authenticity and local identity command a premium.

Operationally, luxury assets require a shift toward total asset optimisation—maximising revenue per square metre through F&B, events, retail, and daytime activation, while simultaneously deploying technology and process efficiencies to mitigate cost inflation. Ultimately, the luxury segment offers one of the most attractive risk-adjusted profiles in European hospitality—but only for investors who approach it as an active, experience-driven platform rather than a passive real estate play.

Extended Stay Hotels

The New Favourite Among Developers

The extended stay sector is rapidly emerging as one of the most structurally supported and institutionally attractive segments within European hospitality, combining strong growth momentum with a fundamentally resilient operating model. As illustrated, the asset class is projected to expand significantly, with market volume growth exceeding 28% by 2033 and transaction activity accelerating sharply year-on-year. This growth is not driven by cyclical recovery, but by clear structural shifts in demand—longer stay durations, hybrid travel patterns, and the increasing overlap between living and travelling which are redefining accommodation needs across both corporate and leisure segments.

From an investment perspective, the sector offers a materially more defensive risk profile compared to traditional hotels. The “commercial living” model introduces a level of flexibility that is rarely available in hospitality, allowing assets to operate across multiple demand segments and, in some cases, providing fallback optionality toward residential use. This adaptability enhances liquidity and exit strategies while reducing exposure to short-term demand volatility. Combined with longer average lengths of stay and a diversified customer base-including corporate, relocation, and leisure guests - this results in more stable and predictable income streams.

Extended Stay asset class is projected to expand significantly, with market volume growth exceeding 28% by 2033 and transaction activity accelerating sharply year-on-year

Operationally, extended stay assets demonstrate superior efficiency and margin resilience. With occupancy levels often exceeding 80% and GOP margins above 60% in well-performing locations, the model benefits from lower staffing intensity, simplified service structures, and more efficient use of space. This lean operating framework is particularly advantageous in the current European environment, where labour costs are rising structurally.

The ability to maintain high profitability with lower operational complexity positions the sector as a strong hedge against margin compression affecting traditional hotel models.

Equally important is the sector’s alignment with modern travel behaviour. The rise of remote work, digital nomadism, and “workation” lifestyles has created sustained demand for accommodation that offers both functionality and comfort over longer periods. Extended stay products cater directly to these needs, providing space, flexibility, and a residential feel that traditional hotels struggle to replicate. This alignment with long-term behavioural trends—not just temporary shifts—underpins the durability of demand and reinforces the sector’s long-term growth trajectory.

For investors, the opportunity lies in capturing scale within what remains a fragmented and underpenetrated market.

By combining prime locations with efficient operating platforms and targeted branding strategies, investors can unlock both stable income and capital appreciation. Early movers who establish platforms and build operational expertise will be best positioned to benefit from the ongoing institutionalisation of the sector. In this context, extended stay is not simply a niche within hospitality-it is increasingly becoming a core pillar of European real estate investment strategies

Branded Residences

Enabler of Luxury Hotel Developments

Branded residences have evolved into one of the most powerful value-enhancement tools within European luxury hospitality, fundamentally reshaping development economics and investor returns. They act as a critical financing bridge in an environment where traditional hotel funding has become more constrained—unlocking early capital through pre-sales and significantly reducing reliance on debt. This ability to recover capital upfront, often through structured payment schedules before project completion, materially improves project liquidity and lowers development risk. At the same time, branded residences introduce multiple revenue streams: immediate sales proceeds, ongoing management and service fees, and additional income generated through rental programmes when units are placed into hotel inventory.

The pricing premium associated with branded residences is a key driver of their attractiveness. Globally, these assets consistently command premiums of 20–35%, with some markets exceeding 40%, driven by brand equity, service standards, and perceived long-term value . This premium is not purely theoretical—it translates directly into higher project margins and stronger exit valuations. Importantly, branded residences also demonstrate superior value retention during downturns, reflecting the resilience of demand from high-net-worth buyers. In supply-constrained European markets, where prime locations and development opportunities are limited, this pricing power becomes even more pronounced, reinforcing the segment’s role as a capital-efficient enhancement to luxury hotel projects.

Opportunity lies in recognising branded residences not as an add-on, but as a core component of luxury development strategy

Demand fundamentals further strengthen the investment case. The global ultra-high-net-worth population is projected to grow by over 28% between 2023 and 2028, alongside a broader expansion of affluent consumers seeking lifestyle-oriented investments rather than purely financial assets . Branded residences sit precisely at this intersection, offering both a tangible asset and an experiential product. This dual appeal is increasingly attracting institutional capital and family offices, with over 12% actively targeting the segment*. The growth is not limited to traditional markets—while hubs like Dubai and North America remain dominant, Europe is emerging as a key frontier due to its scarcity of product and strong global appeal.

From a strategic perspective, the true strength of branded residences lies in their ability to integrate into a broader hospitality ecosystem. Whether fully integrated with hotels or developed as hybrid models, they enable cross-utilisation of services, amenities, and infrastructure, creating synergies that enhance both residential and hotel performance. This ecosystem approach where owners benefit from hotel services while contributing to occupancy, F&B, and ancillary revenue - drives higher overall asset productivity. However, success depends heavily on early alignment between developer, operator, and brand, as well as careful planning of product mix, operational design, and target market positioning.

For investors, the opportunity lies in recognising branded residences not as an add-on, but as a core component of luxury development strategy. When executed correctly, they can significantly enhance returns, de-risk development, and create differentiated, high-barrier assets in competitive markets. However, they also introduce complexity—brand requirements, operational standards, and governance structures must be carefully managed to protect long-term value.

Ultimately, branded residences represent a convergence of real estate, hospitality, and brand equity, offering one of the most compelling pathways to generate outsized returns in the evolving European luxury hotel investment landscape

Family-Owned Hotels

Largest Transaction Trend in Decades Waiting Around the Corner

The next major shift in the European hotel investment landscape will be driven by a generational transition: a growing number of owner-operators will no longer have successors willing or able to continue running their businesses. Across Southern Europe in particular, many hotels remain in the hands of first- or second-generation families whose operating models are deeply personal and relationship-driven. As these owners approach retirement, and with younger generations often pursuing different careers, a structural supply of assets is emerging—well-located, established hotels that lack the capital, branding, and professional management needed to remain competitive.

This transition is already reshaping transaction activity. Markets such as France, Spain, Italy, Greece, and Portugal are seeing increasing volumes not only because of strong tourism fundamentals, but because ownership fragmentation is beginning to unwind. These assets frequently come with clear repositioning potential: underinvested physical product, limited distribution reach, and suboptimal pricing strategies. For institutional investors and experienced operators, this creates an opportunity to acquire at attractive entry points and unlock value through refurbishment, rebranding, and operational optimisation.

However, the opportunity is not without complexity. Southern European markets require deep local knowledge, patience, and execution capability. Legal structures can be opaque, permitting timelines unpredictable, and assets may lack full compliance or documentation. Successful investors are therefore those who approach the strategy as platform-driven rather than transactional—building local teams, establishing relationships with authorities and contractors, and underwriting timelines conservatively.

Over the longer term, this trend represents the gradual institutionalisation of European hospitality, mirroring the evolution seen in the United States decades earlier. Fragmented, family-owned assets will increasingly transition into professionally managed, branded, and scaled portfolios. Investors who can navigate the current phase of complexity will be well positioned to capture outsized returns, as they participate in a multi-decade shift from legacy ownership to institutional capital and modern operating models.

Debt Market

A shift toward debt strategies as refinancing becomes the centre of attention and investors seek higher risk adjusted returns across the capital stack

The European hotel investment environment saw a notable change emerge a few years ago across the capital stack: the most attractive risk-adjusted returns were increasingly found in debt rather than equity. This reflected a market where equity pricing remains relatively elevated, while operating fundamentals—particularly margins are under structural pressure from labour costs and inflation. At the same time, regulatory changes are reshaping lending dynamics. With the implementation of Basel III, banks are required to hold more capital against real estate loans, effectively tightening lending conditions, reducing loan-to-value ratios, and increasing borrowing costs for hotel investors. As a result, traditional bank lending has become more selective, creating space for private credit to expand.

Private credit has therefore gained significant traction within the hospitality sector, often marketed as a “best of both worlds” solution—offering equity-like returns with debt-like risk. In many cases, it has been positioned almost as a miracle product within real estate capital markets. However, this narrative deserves scrutiny. The rapid growth of private debt—projected to expand significantly in the coming years and already becoming a cornerstone of institutional portfolios - has in some cases been accompanied by weaker underwriting discipline, optimistic business plans, and insufficient attention to realistic exit assumptions, particularly around refinancing in a higher-rate or volatile environment. The perception of safety can therefore be misleading if not supported by active asset management and rigorous credit analysis, especially if the underwriting assumes yield compression with tight and unflexible holding periods.

The opportunity set within hotel private credit remains compelling, particularly in transitional lending, refinancing, and generational ownership transitions. However, these opportunities require a level of expertise that goes beyond financial structuring. Hotel performance is dynamic, and while the sector benefits from inflation-hedging characteristics and strong demand fundamentals, it is also exposed to operational volatility.

Ultimately, while hotel private credit represents a highly attractive and flexible investment strategy, it is not immune to market cycles, which is indication that private credit is in verge of maturing. The current environment—characterised by abundant liquidity, competitive lending, and a strong narrative around private credit—has, in some cases, created complacency. When the next market shock occurs, whether through macroeconomic tightening, refinancing constraints, or geopolitical disruption, those strategies built on aggressive assumptions, passive monitoring, and unrealistic exit scenarios are likely to be exposed. The real competitive advantage will lie with investors who combine comprehensive underwriting, active asset management, ESG-aligned financing strategies, and the flexibility to move across the capital stack.

At the same time, ESG considerations and sustainability-linked financing are increasingly influencing the lending landscape. Assets lacking strong ESG credentials may face challenges in securing financing, while green loans and sustainability-linked debt structures are gaining traction as preferred funding solutions. This introduces both opportunity and risk: while green financing can improve pricing and access to capital, it also adds another layer of underwriting complexity, where compliance and future regulatory alignment must be carefully assessed. Investors relying on superficial ESG positioning without operational substance may face refinancing challenges as standards tighten.

Family Offices

Growing influence of private wealth reshaping hotel investment through long term ownership flexibility and direct operational involvement

Family office capital has emerged as one of the most dynamic and influential forces in the European hotel investment landscape, fundamentally reshaping how capital is deployed across the sector. High-net-worth individuals (HNWIs) are no longer marginal participants but increasingly dominant buyers, with transaction share rising to approximately 14%* in recent years and acquisition activity consistently outpacing dispositions. This shift reflects not only growing allocation to hospitality as an asset class, but also a broader structural evolution in how private wealth engages with real estate—moving from passive allocation toward direct ownership and operational involvement.

Family offices are increasingly combining forces into multi-family platforms bringing institutional expertise and structured investment strategies to what was once fragmented individual ownership.

The scale of this trend is underpinned by the rapid expansion of the family office universe itself. Globally, the number of family offices continues to grow at pace, supported by increasing wealth creation and intergenerational capital transfer. As these platforms mature, many are transitioning from opportunistic investors into fully institutionalised operators, building in-house capabilities across investment, development, and asset management. The result is a hybrid investor profile combining the sophistication of institutional capital with the flexibility and long-term orientation of private ownership.

What distinguishes family offices most clearly in the current market environment is their structural advantage in capital deployment. Unlike private equity funds, they are often not constrained by fund lifecycles or exit timelines, allowing them to underwrite investments with a genuinely long-term perspective. In a market characterised by bid-ask spreads, refinancing uncertainty, and volatile macroeconomic conditions, this permanence becomes a decisive advantage. Family offices can hold, reposition, and stabilise assets through cycles, rather than being forced to transact at suboptimal moments.

Equally important is their agility and risk tolerance. Family offices are often among the first to deploy capital following market dislocations, acting ahead of institutional investors who require pricing clarity and committee-driven approvals. Their ability to accept personal recourse, structure flexible financing, and engage in complex or off-market transactions allows them to access opportunities that are less accessible to more rigid capital structures. This is particularly relevant in still fragmented European markets, where deal execution often depends on speed, relationships, and bespoke structuring.

Strategically, family offices are not a homogeneous investor group, and this diversity strengthens their role in the market. European family offices tend to favour direct ownership and curated, often upscale or lifestyle-oriented assets, while others pursue platform-building strategies or co-investments at scale. This breadth of approach—ranging from boutique luxury acquisitions to large, vertically integrated portfolios creates a resilient and multi-layered demand base within the European hotel sector. As a result, family office capital is not only growing in volume but also shaping the competitive dynamics of the market, increasingly setting pricing, influencing asset strategies, and redefining what constitutes “core” hospitality investment in Europe.